Insights

Your Borrower Just Defaulted. Do You Know Your Options?

20 April 2026 7 minutes read

When a borrower starts missing payments, or when your own company’s debt obligations become unmanageable, the instinct is often to move fast: accelerate the loan, push for collateral enforcement, or brace for bankruptcy proceedings. But in Indonesia, that instinct can cost you.

Corporate financial distress in Indonesia is accelerating. In 2024, Indonesia’s five Commercial Courts recorded 538 PKPU filings and 92 bankruptcy petitions, a combined 630 cases for the year. By 2025, the pressure intensified further: filings across four of the five courts surged by at least 31%, driven by unresolved post-pandemic debt, rising operational costs, and the ripple effect of high-profile corporate collapses such as Sritex. For CFOs, general counsel, and investment officers with Indonesia exposure, this is not a background trend. It is a frontline operational risk.

At the centre of this landscape is PKPU — Penundaan Kewajiban Pembayaran Utang, or Delay of Payment, Indonesia’s court-supervised debt restructuring mechanism. Understanding how it works, and when to act, should be non-negotiable for any decision-maker operating in this market.

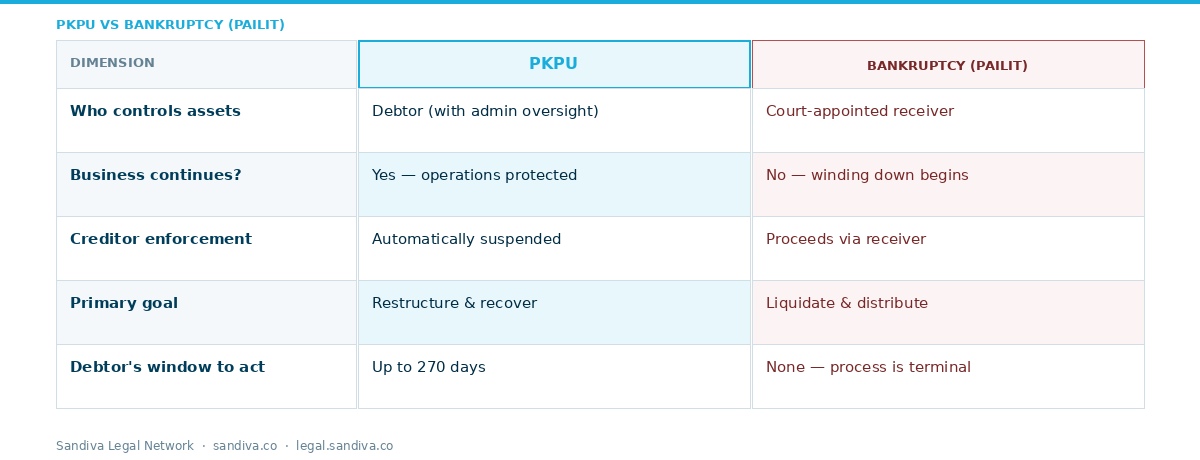

What PKPU Is — and What It Is Not

PKPU is often mischaracterized as a softer form of bankruptcy. It is not. The two mechanisms have fundamentally different objectives, power structures, and outcomes for all parties involved.

The critical distinction: in PKPU, the debtor retains operational control of the business, subject to oversight by a court-appointed administrator. In bankruptcy, a receiver takes over, and the path leads to liquidation. For creditors, this matters enormously: a functioning business is far more likely to generate recoveries than an asset fire-sale.

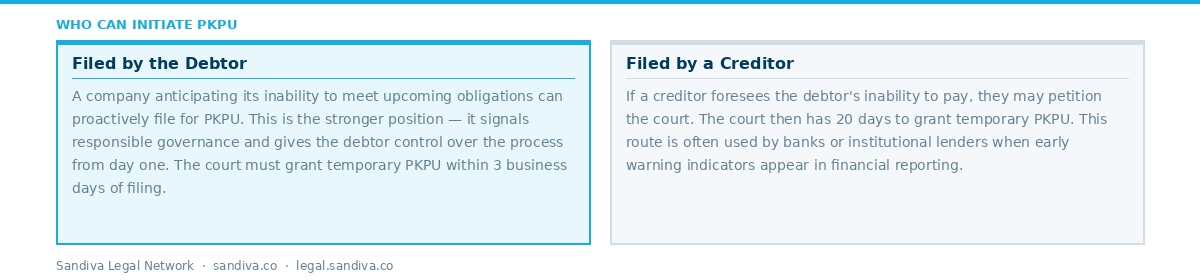

Who Can Initiate PKPU — and When

PKPU can be filed by either the debtor or a creditor under Law No. 37 of 2004. This dual access is intentional: the law recognizes that financial distress affects both sides, and that early intervention benefits everyone.

The timing of filing is critical. Companies and creditors that engage PKPU early — before the situation becomes adversarial — consistently achieve better negotiation outcomes, more creditor participation, and more durable restructuring plans. Between January and 23 May 2025, Indonesia’s five Commercial Courts already recorded 163 PKPU petitions and 71 bankruptcy petitions — a combined 207 cases in under five months. ⁴ Waiting until enforcement actions have been taken narrows the options for everyone.

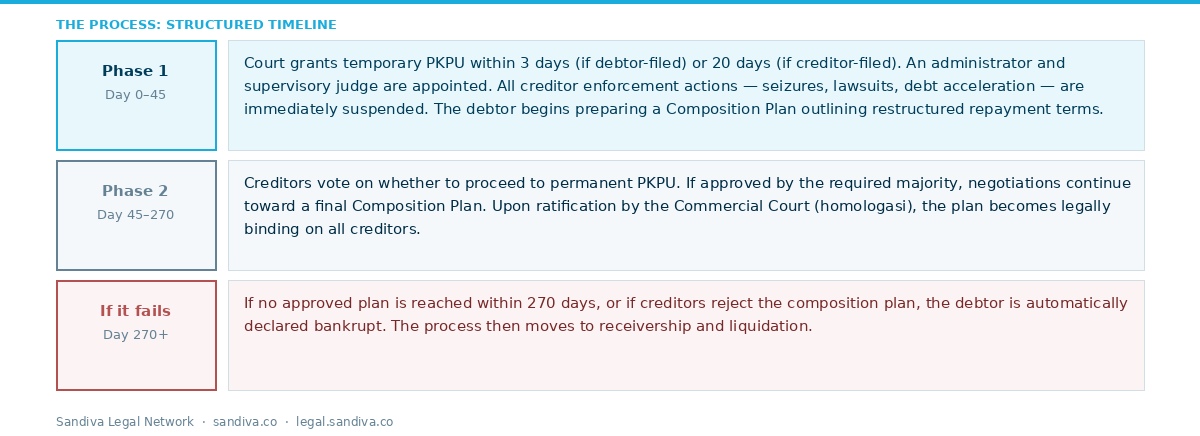

The Process: A Structured Timeline

PKPU operates on a legally defined timeline with clear milestones. For decision-makers, understanding this sequence is essential for planning your response strategy.

The Creditor Approval Threshold

Understanding the voting mechanics is essential for creditors — particularly those managing significant claim positions.

For a Composition Plan to be approved and ratified, it must secure a dual majority: more than half of the unsecured (concurrent) creditors present at the hearing, representing at least two-thirds of the total unsecured claim value; and more than half of the secured creditors present, representing at least two-thirds of total secured claim value.

The Administrator: Why This Appointment Decides Everything

The administrator (pengurus) is the most consequential variable in any PKPU process. Appointed by the court, the administrator sits between debtor and creditors — not as an adversary to either, but as a structured negotiation facilitator with legal authority.

Key powers of the administrator:

- No significant asset management or disposal by the debtor is permitted without the administrator’s written consent

- The administrator supervises all legal acts of the debtor during the PKPU period

- The administrator files periodic reports to the supervisory judge every three months

- The administrator facilitates creditor negotiations and composition plan development

In practice, administrators who combine legal expertise with genuine financial and business acumen produce significantly better outcomes. Cases where administrators operated purely procedurally — focused on compliance rather than deal-making — have shown lower homologation rates and higher post-PKPU business failure rates.

For Creditors: What PKPU Means for Your Position

If your organization has loan exposure to an Indonesian debtor that has entered or is approaching PKPU, your immediate priorities should be:

- Ensure your claim is formally registered and verified in the proceedings — unregistered creditors risk exclusion from the distribution

- Assess your classification: secured vs. unsecured has direct implications for your voting rights and recovery priority

- Engage counsel with Indonesian insolvency experience immediately — the 45-day window is not long enough to be reactive

- Evaluate the proposed Composition Plan against liquidation recovery scenarios before voting

- For foreign creditors: Indonesia does not recognise foreign insolvency judgments, which means local proceedings require local representation

Warning Indicators: When to Act

Both debtors and creditors should treat the following as signals that PKPU-related counsel is needed immediately:

- Debt service coverage ratio falling below 1.0x for two or more consecutive quarters

- Formal notices of default or acceleration received from any creditor

- Creditors beginning to take enforcement action on secured collateral

- Auditor qualifications or going-concern notes appearing in financial statements

- Informal creditor discussions breaking down without a framework agreement

- Awareness of another creditor preparing to file a bankruptcy petition

The window between financial stress and formal insolvency proceedings is often shorter than management teams expect. Acting before the petition is filed — not after — is where the most meaningful options exist.

How Sandiva Can Help

Sandiva advises both debtors and creditors — including foreign institutional lenders — across the full PKPU and insolvency spectrum: from pre-filing strategy and administrator selection to composition plan negotiation, cross-border creditor representation, and collateral enforcement.

If your organization is dealing with a distressed exposure in Indonesia — or if you are a business owner navigating financial pressure — we are available for a confidential, no-commitment initial discussion.

_________________________________________________________________________________________

DATA SOURCES

¹ Hukumonline. (January 2025). “Menurun di Tahun Lalu, PKPU dan Kepailitan Diprediksi Meningkat di 2025.” Data compiled from SIPP (Sistem Informasi Penelusuran Perkara) across Pengadilan Niaga Jakarta Pusat, Medan, Semarang, Surabaya, and Makassar, January–December 2024. Available at: hukumonline.com

² Law No. 37 of 2004 on Bankruptcy and Suspension of Debt Payment Obligations (UU Kepailitan dan PKPU), Article 228(6). Available at: peraturan.bpk.go.id

³ Bisnis.com. (2 March 2026). “Tren PKPU dan Pailit Melonjak 31% pada 2025, Alarm Bahaya dari Sektor Korporasi.” Data from SIPP across PN Surabaya, Semarang, Medan, and Makassar (PN Jakarta Pusat data unavailable at time of reporting; actual national total may be higher). Available at: kabar24.bisnis.com

⁴ KONTAN. (23 May 2025). “Perkara PKPU & Kepailitan Menurun hingga Mei 2025, Bagaimana Dampaknya pada Ekonomi?” Data from SIPP across five Pengadilan Niaga, January–23 May 2025. Available at: nasional.kontan.co.id

This article is intended for general informational purposes only and does not constitute legal or financial advice. For advice specific to your situation, please consult Sandiva directly.